NMC Insurance Solutions

We don’t look at insurance in isolation. We look at your entire financial picture—investments, retirement, estate planning, taxes, and protection—so every recommendation fits into a thoughtful, coordinated plan. Our goal is simple: help you build a strong future while protecting the people and life you care about most.

Insurance Solutions We Offer

-

TERM INSURANCE

Affordable coverage designed to protect your family for a specific period of time. -

INDEXED UNIVERSAL LIFE

Flexible protection that can support long-term growth and tax-advantaged retirement income. -

PLANNING FOR YOUR CHILD’S FUTURE

A long-term strategy designed to build protection and financial flexibility for the next generation. -

LONG-TERM CARE

Coverage that helps manage the cost of care while protecting your assets and family. -

DISABILITY

Income protection that helps replace your earnings if illness or injury prevents you from working.

-

ANNUITIES

Retirement income solutions designed to provide stability, guarantees, and peace of mind.

-

BUSINESS KEY PERSON

Protection that helps businesses manage the financial impact of losing a critical team member.

-

BUSINESS BUY-SELL

A structured solution that ensures smooth ownership transitions between business partners.

-

BUSINESS INSURANCE STRATEGIES

Tax-efficient solutions designed to reward, retain, and protect key employees and owners.

Term Insurance

Term insurance is a cost-effective way to protect what matters most. It can be used to:

Provide financial support to your family if something happens to you

Ensure a surviving partner isn’t burdened with major expenses like a mortgage

Create financial stability during key life stages (raising children, paying off debt, etc.)

We’ll help you determine if term insurance fits your needs—and if so, find the right structure and coverage amount.

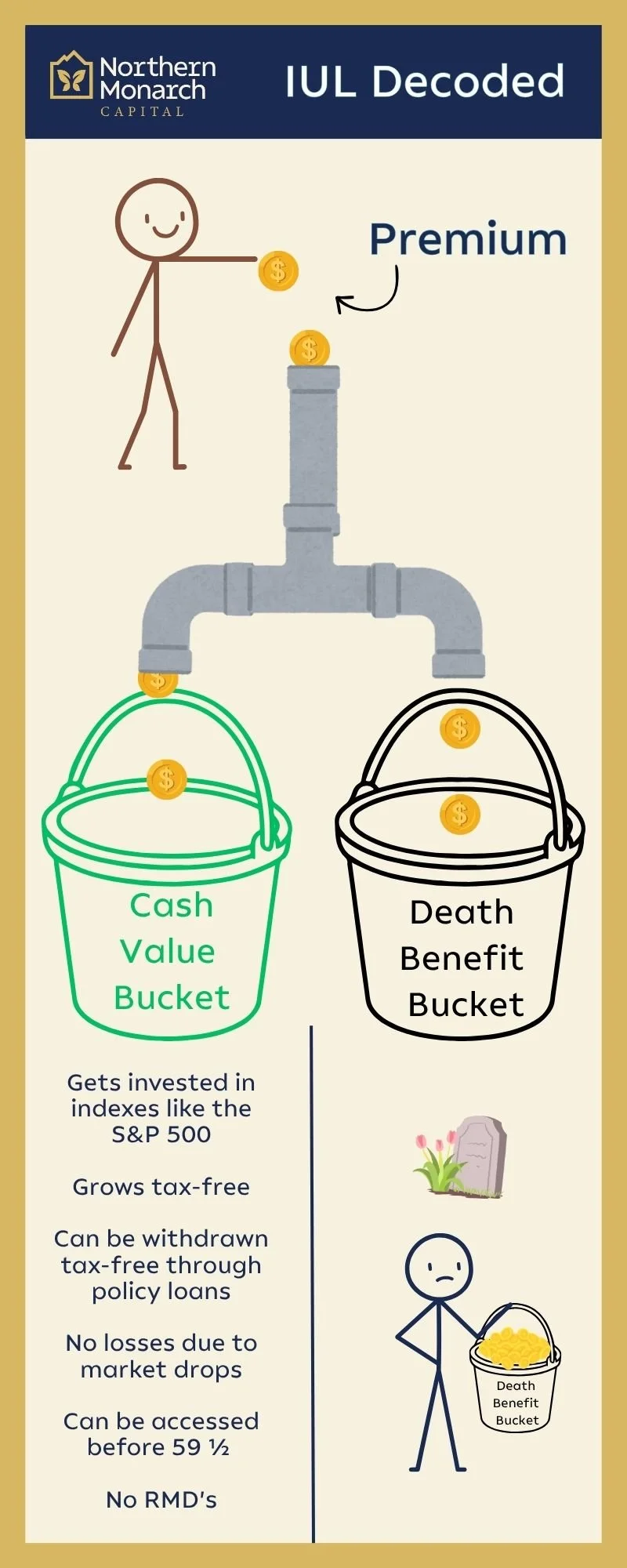

Indexed Universal Life (IUL)

When properly designed, an IUL can serve multiple roles within a financial plan.

It offers:

Tax-advantaged access to funds in retirement

Downside protection (your account won’t lose value due to market declines)

Upside potential tied to market performance

A death benefit to protect your family

Optional living benefits, such as chronic illness or long-term care riders

Unlike many retirement accounts, an IUL can provide flexibility:

No required minimum distributions (RMDs)

No strict contribution limits like qualified plans

No age restriction for accessing funds (when structured properly)

That said, IULs are not one-size-fits-all. Cost and effectiveness depend heavily on how the policy is structured and funded. When done incorrectly, they can be inefficient. When done well, they can be a powerful planning tool.

If you’re curious, we’ll walk through it together and determine whether it truly fits your situation.

Planning for Your Child’s Future - Juvenile IUL

A juvenile IUL is a long-term strategy designed to give children a financial head start while also providing lifelong protection.

It can help:

Build tax-advantaged cash value over time

Provide flexibility for future needs like a first car, home purchase, wedding, or other life goals

Create a financial resource they can access later in life

Establish coverage early, helping secure insurability based on their health at a young age

Unlike some education-specific accounts, these funds are not restricted to education expenses, giving your child the flexibility to use them wherever life takes them. In many cases, life insurance assets are also treated differently than traditional college savings accounts in financial aid calculations, which may help preserve eligibility for certain forms of aid.

When structured properly, this can be a powerful tool to support your child’s future while maintaining flexibility as their path evolves.

Long-Term Care

As people live longer, the likelihood of needing care increases. According to the U.S. Department of Health and Human Services, 7 out of 10 people will require some form of long-term care during their lifetime.

This care can include:

In-home assistance

Assisted living

Skilled nursing facilities

Long-term care coverage helps protect your assets and reduces the financial and emotional burden placed on your family.

It can be purchased on its own or as a part of an IUL policy. The fantastic benefit of that strategy is the ability to not use it if you don’t end up needing it. The funds that would have gone toward long-term care simply pass to your beneficiaries.

Disability Insurance

Your ability to earn an income is one of your most valuable assets.

Disability insurance helps:

Replace a portion of your income if you’re unable to work

Cover essential expenses during recovery

Protect your long-term financial plan from unexpected setbacks

Many people insure their home and belongings—but not their income. This coverage helps close that gap.

Annuities

Annuities are designed to provide predictable, reliable income in retirement, helping reduce the stress of market uncertainty and longevity risk.

Depending on the type, annuities can offer:

Guaranteed income for life or a set period

Protection from market downturns

Tax-deferred growth

Optional riders for income, inflation protection, or long-term care needs

Annuities can play an important role in creating a stable income foundation, allowing your other investments to remain positioned for growth. We’ll help you determine if—and how—they fit into your overall retirement strategy.

Key Person Insurance

For business owners, certain individuals are critical to operations, revenue, or relationships.

Key person insurance:

Provides funds to help the business recover from the loss of a key employee or owner

Helps cover lost revenue, hiring costs, or transition expenses

Supports business continuity during a difficult time

It’s a strategic way to protect the stability and value of your business.

Buy-Sell Insurance

A buy-sell agreement funded with insurance creates a clear, financially supported plan for ownership transitions.

It helps:

Ensure remaining owners can buy out a departing partner’s share

Provide fair compensation to the departing owner or their family

Prevent disputes or financial strain during an already difficult time

This is essential planning for any business with multiple owners.

Business Insurance Strategies

These strategies are designed to help business owners attract, reward, and retain key employees in a tax-efficient way.

Common approaches can:

Provide valuable benefits to key team members

Offer flexibility compared to traditional qualified plans

Create incentives for long-term retention

Support business succession and continuity planning

Whether you’re looking to reward leadership, strengthen your team, or create a more competitive benefits offering, we can design a solution aligned with your business goals.